Past-due customers do not wake up excited to call collections. When they do engage, the window is small: understand the balance, ask one or two questions, and either pay or set up a plan. That window starts closing the moment they have to repeat themselves.

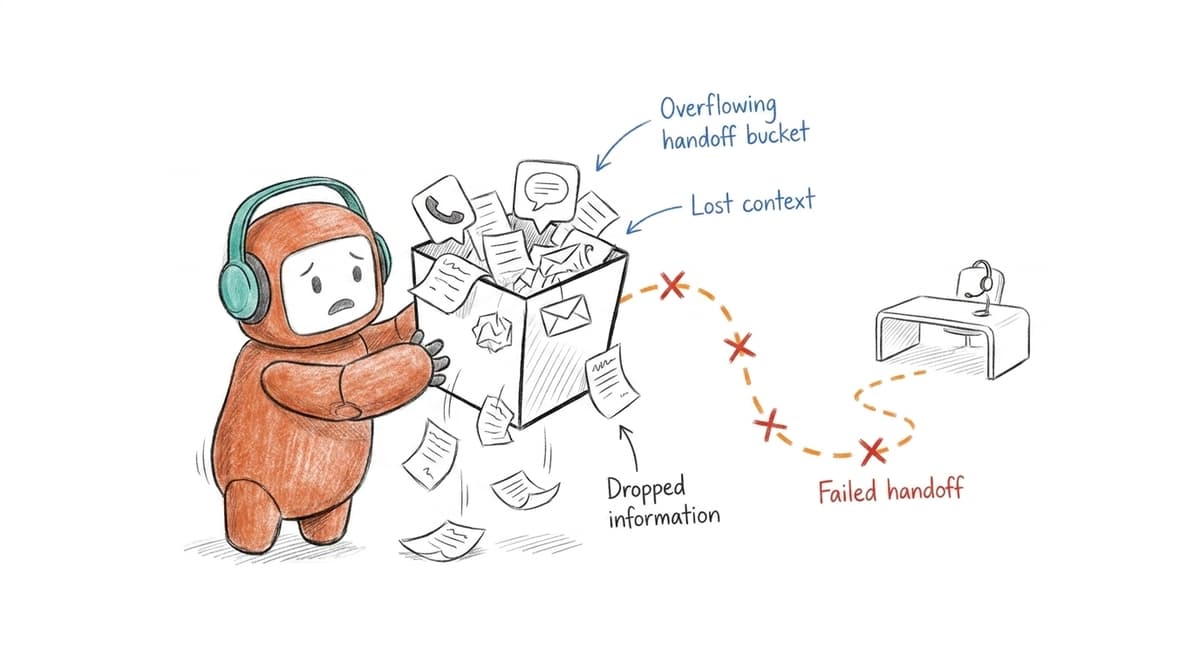

Every transfer, repeated question, and missing note turns a ready-to-pay caller into a repeat contact. The biggest call escalation process mistakes are not simple routing errors. They are context breaks: AI handles the easy part, then the hard moment lands on a human who does not know what just happened.

For collections and payment recovery teams, that break costs real cash. The customer was already on the line.

The fix starts before transfer: define what AI must capture, what triggers a human handoff, and how the next agent receives the full conversation.

Key Takeaways:

- Fix payment recovery escalation by deciding exactly when AI should stop and a person should take over.

- Treat payment intent as a priority signal, not just another support queue event.

- Use hard thresholds for sentiment, dispute language, payment-plan requests, and repeat failed authentication.

- Measure escalations by recovered balances, right-party contact, and call continuity, not just transfer volume.

- Build one shared thread across voice, SMS, email, and chat so customers don't repeat themselves.

- Keep compliance rules inside the workflow before contact attempts and sensitive messages go out.

Why Payment Recovery Calls Break During Escalation

The common assumption is that escalation means failure. I don't buy that. In payment recovery, escalation is often the exact moment where revenue is still recoverable. The mistake is treating every escalation as an exception instead of designing it as part of the normal path from contact to resolution.

The Payment Window Is Shorter Than the Queue

A collections manager opens the Monday dashboard at 8:30 a.m. and sees 1,400 past-due accounts loaded for outreach. By 10:00, the AI has reached hundreds of customers, but 47 people who asked for payment plans are sitting in a generic support queue. Some are marked "needs agent," some are tagged "billing question," and some have no tag at all. By lunch, a few customers have already stopped responding.

That scene is where most call escalation process mistakes start. Not with bad intent. Not with a lazy team. The process was built like a support queue, where waiting is annoying but survivable. Payment recovery is different. A customer who says "I can pay half today" isn't just asking a question; they're giving you a live recovery signal that decays by the minute.

Consumer debt rules also raise the stakes. The CFPB's Regulation F materials make clear that communication practices, disclosures, and contact behavior matter in debt collection workflows. Payment teams don't just need faster escalation. They need escalation that knows when the conversation has moved from routine explanation to regulated recovery action.

Fragmented Tools Turn Handoffs Into Rework

Fragmented escalation looks manageable from far away. A voice bot answers the call, a dialer records the attempt, a CRM stores the account, and a helpdesk catches the ticket. The problem shows up inside the handoff. Nobody sees the same version of the customer conversation.

Think of a payment recovery call like a relay race run inside a narrow hallway crowded with filing cabinets. The AI starts with speed, but the handoff lane is blocked: one cabinet holds call notes, another holds SMS history, another holds the payment-plan workflow, another holds compliance review. The baton doesn't drop because the runners are careless. It drops because nobody can swing their arm without hitting a drawer that belongs to a different team.

There is a fair argument for keeping specialist tools. Dialers are familiar. Helpdesks are already installed. CRMs remain the customer record, and they should. That's a reasonable read of the operational reality. The deeper problem is asking a customer in a tense payment conversation to pay the price for your internal architecture.

Escalation Feels Small Until It Hits Compliance

Rules that live outside the conversation flow turn ordinary escalations into compliance exposure. Time windows, consent status, opt-outs, dispute language, and required disclosures can't depend on memory or a note buried three screens away. The FCC's guidance on telemarketing and robocalls is a useful reminder that automated outreach sits inside a rule-heavy environment, not a blank canvas.

The emotional cost is real too. Your agents get the worst version of the customer: already contacted, already confused, already asked to repeat themselves. Frankly, that wears people down. For the customer, the experience feels like the company is organized around collection activity, not resolution.

The handoff isn't an administrative step. It is the moment where the recovery process either earns the next sentence from the customer or loses it.

How to Fix Call Escalation Process Mistakes

Fix call escalation process mistakes by designing escalation around customer intent, account risk, and conversation state. The better model is simple: AI handles structured work, humans handle judgment, and both operate from the same conversation record. Payment recovery improves when escalation is planned before the call starts.

The goal is not to push every hard conversation to a person. That would erase the capacity gain from automation. The goal is to know, in plain operational terms, which moments need a person and which moments need a better automated path. Payment teams should be able to explain that rule in one sentence.

Audit the Handoff Before You Rewrite the Script

Before rewriting any script, pull the last 100 escalated payment calls and ask five diagnostic questions of each one. Did the customer ask about a payment plan, dispute the balance, show anger, fail authentication twice, or request an agent? What happened in the next 10 minutes? Did the customer reach the right person? Did the agent see the call summary? Did the account record update before the follow-up message went out?

That audit gives you a real diagnostic instead of opinions. Two thresholds matter. If more than 20% of escalations require the agent to ask the customer to repeat the balance, account status, or previous promise, the issue is not agent training, it is missing context. If more than 10% of payment-plan requests wait over 15 minutes for human review during business hours, the queue is treating recovery intent like a normal ticket.

Use a simple review sheet:

- Trigger: Why did the call escalate?

- Timing: How many seconds passed between trigger and handoff?

- Context: What did the agent receive before speaking?

- Outcome: Payment, plan, dispute, promise, abandonment, or follow-up needed.

- Leak: Where did the process lose information or momentum?

Numbers matter here. A team can tolerate some delay on a general billing question. A customer with current payment intent should not sit behind password resets and address changes. The audit forces that distinction into the open, and it usually catches the hidden mistakes faster than a dashboard built around average handle time.

Define Human Takeover With Thresholds, Not Vibes

"Send to agent when needed" is not a rule. It is a hope. A payment recovery escalation process needs hard thresholds, defined as the exact triggers that require human takeover, then tested against real calls. The most useful triggers are not fancy. They are observable in conversation.

Set the first version aggressively enough to protect the customer experience, then loosen only where the data proves you can. I prefer starting with four mandatory takeover points: explicit dispute language, negative sentiment above a defined level, payment-plan negotiation outside approved options, and repeated authentication failure. If a customer says, "That balance is wrong," the AI should not keep trying to close. If the customer says, "I can pay Friday but not today," the workflow needs either an approved plan path or a person who can judge the exception.

A practical rule set might look like this:

- Dispute language: Escalate immediately when the customer challenges the debt, amount, identity, or prior payment.

- Payment-plan exception: Escalate when the requested plan sits outside approved terms.

- High-risk emotion: Escalate when frustration or distress appears twice in the same conversation.

- Authentication failure: Escalate after two failed attempts or any mismatch involving sensitive account details.

- Customer request: Escalate when the customer asks for a person, unless the request is clearly accidental.

Some teams prefer letting the AI keep trying because human capacity is limited. That is a legitimate constraint, not a bad-faith argument. Still, the constraint should change the routing model, not the trigger definition. If there are not enough agents for high-intent escalations, route by recovery value, risk, and customer tier. Don't hide capacity problems inside vague automation rules.

Route Payment Intent Differently From Support Intent

Why do collections teams keep losing recoverable balances to their own queue design? Because a customer asking, "Can I pay now?" lands in the same lane as "Where do I update my email?" Both are service events, but only one has an active recovery window. Treating them the same is one of the most common call escalation process mistakes in collections teams.

Build routing around what the customer is trying to do, not the channel they came from. Voice, SMS, chat, and email are just entrances. The intent is the real work. If a customer starts on a voice call, asks for a payment link by SMS, then replies with a question about fees, the escalation logic should follow the same thread across all three moments.

A basic intent model should split recovery conversations into five lanes:

- Pay now: Move toward payment completion or secure payment handoff.

- Set up a plan: Offer approved plan options or escalate exceptions.

- Dispute balance: Stop collection-style persuasion and route to the right review path.

- Can't authenticate: Protect the account and move to a controlled human process.

- Needs empathy: Route to a trained agent when the customer shows hardship, confusion, or distress.

The hidden connection is that better escalation can improve both recovery and agent morale. Agents don't mind hard conversations when they receive them with context and purpose. They hate being dropped into a call where the customer is angry and the system says only, "transferred from bot." That is not support. That is cleanup.

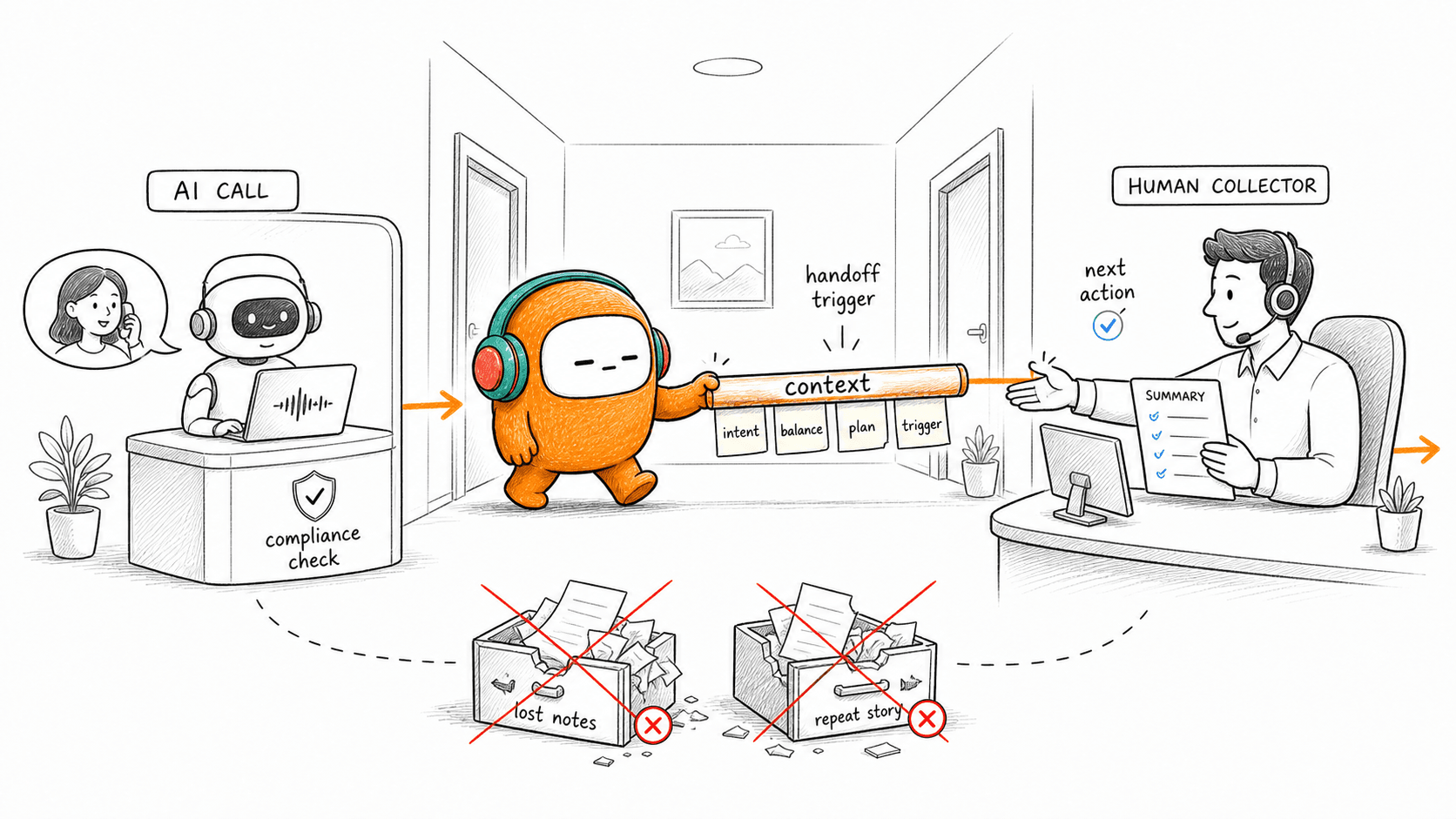

Give Agents the Full Conversation, Not a Summary Fragment

A useful escalation record includes the full conversation thread, the reason for handoff, customer intent, account context, prior outreach, and suggested next action. A summary alone is not enough. Summaries compress, and payment recovery depends on the details customers use to explain trust, hardship, and timing.

Before approving any escalation design, run one test: can a human agent read the handoff packet for 20 seconds and continue the conversation without asking the customer to restart? If no, the packet is too thin. If the agent needs to open more than two systems to act, the workflow is too fragmented. If the agent can't tell whether an SMS follow-up already went out, the process is not safe enough for high-volume recovery.

The handoff packet should include:

- Customer identity and account status from the approved system.

- Conversation transcript across channels, not just the final call segment.

- Escalation trigger in plain language.

- Customer's last stated intent such as pay now, plan, dispute, hardship, or agent request.

- Allowed next actions based on policy, approval rules, and account state.

We learned this the hard way in automation projects: the "small" missing field is usually the field the human needs most. A customer says, "I already told the bot I can pay on Friday," and the agent can't see it. The customer hears that as incompetence. The agent experiences it as preventable friction. Both are right.

The handoff design is easier to judge when you can see a real payment recovery flow in motion, so book a demo with the team that implements it.

Measure Escalation by Resolution, Not Transfer Rate

Transfer rate is a weak metric by itself. A low transfer rate can mean the AI is doing excellent work. It can also mean the AI is trapping customers in conversations that should have moved to a person. Payment recovery teams need metrics tied to resolution and risk, not just containment.

Use a two-level scorecard. The first level tracks operational speed: trigger-to-agent time, agent acceptance time, repeat-question rate, and abandon-after-escalation rate. The second level tracks recovery quality: payment completed, plan created, promise captured, dispute routed correctly, and follow-up sent within the approved window. If transfer rate improves while recovered balance drops, the automation is solving the wrong problem.

Two benchmarks worth setting alarms on: review any escalation path where more than 15% of customers abandon after requesting a person, and review any AI-handled path where customers repeat the same intent three times in one conversation. Those two signals usually expose the same issue from opposite sides. Either escalation is too slow, or the AI is staying in the conversation past its useful limit.

Not every team needs the same thresholds. A low-volume operation with complex accounts may escalate more often and still perform well. A high-volume portfolio with standardized payment plans can automate more of the middle. The deciding factor is not company size. It is how much judgment the next step requires after the customer declares intent.

Keep Compliance Inside the Workflow

Compliance can't sit at the end of the payment recovery process like a final inspection. It has to be checked before the outreach attempt, during the conversation, and again before sensitive messages go out. That requires rules tied to the same workflow the AI and agents are using.

The basic test is uncomfortable but useful: if a regulator asked why a customer received a specific call, message, or follow-up, could your team reconstruct the decision in under 10 minutes? You should be able to see consent status, contact window, opt-out state, script version, escalation trigger, agent action, and final outcome. If the answer requires three exports and a Slack thread, the process is too brittle.

Payment recovery workflows should enforce:

- Consent and opt-out checks before contact attempts.

- Time-window rules based on customer location and policy.

- Approved scripts for sensitive balance or collection language.

- Human approval for higher-risk messages.

- Audit trails that connect the call, message, and agent action.

The honest limitation: strong governance slows a few edge cases. Some messages will wait for approval. Some calls will move to humans earlier than operations leaders prefer. That tradeoff is worth making when the alternative is faster contact with weaker control. In regulated recovery work, speed without proof becomes a cost later.

How Revve Handles Payment Recovery Handoffs

Revve handles payment recovery handoffs by keeping AI conversations, human agents, channels, and compliance controls in one customer operations workspace. The platform is designed for voice, chat, SMS, and email to share one operating record. That means escalation can carry context instead of forcing agents to rebuild it.

Revve is not just a chatbot or a dialer. It runs the recovery conversation across the channels where customers actually respond, then moves the work to a human when the rules say judgment is needed. It also supports cloud and on-prem deployment options depending on the environment.

One Thread Across Voice, SMS, Email, and Chat

Revve's omnichannel conversation management ties voice, SMS, WhatsApp, email, chat, and other supported channels to one customer thread. That matters in payment recovery because the customer rarely stays inside one channel. A call can become an SMS payment link, then an email confirmation, then a human follow-up.

The AI Voice Agent and AI Chat Agent use the same knowledge-grounded automation layer, so teams do not have to rebuild answers and escalation logic for every channel. When a conversation needs a person, Smart Escalation and Full-Context Handoff passes the thread, summary, prior history, and suggested next steps into the human workspace. Revve also keeps human agents in control where judgment or approval is required. That is the right boundary.

Governance Built Into the Recovery Workflow

Revve includes compliance controls and approval workflows for outbound and sensitive customer contact. The platform can check configured rules such as consent status, local time windows, do-not-call restrictions, opt-out requirements, and approval steps before messages are sent. For payment recovery, that keeps governance close to the action instead of buried in a separate review process.

Revve's outbound orchestration also fits recovery work because teams can configure multi-step outreach across calls, SMS, messaging apps, and email. Contacts can be enrolled through CRM sync or CSV import, and each touchpoint remains part of the same customer history. The value is not that AI replaces the recovery team. The value is that AI takes the repetitive contact, routing, and follow-up work, while humans own the moments that need discretion.

Build Escalation Around Resolution, Not Deflection

Call escalation process mistakes are expensive because they hide inside a metric that looks good on the surface. Fewer transfers can look efficient while customers abandon payment, repeat themselves, or land in the wrong queue. Payment recovery needs a different standard.

Design the process around the moment a customer is ready to resolve. Define the triggers. Pass the full context. Route payment intent differently from support intent. Keep the compliance record attached to the conversation. Revve gives enterprise teams the shared workspace, channel coverage, and governed handoff model to make that possible without asking customers to restart the story every time the conversation changes hands.