By 9:12 a.m., the collections queue already holds 480 accounts, and the first mistake happened before anyone picked up a phone. Most teams try to increase payment collections with more dials, longer agent hours, or another reminder tool. That works for a week. Then volume exposes every weak handoff: the customer answers on attempt two, asks one question, gets routed to another team, and the payment moment evaporates.

It feels like a staffing problem. It is usually an operating problem.

A collections workflow is not just a call. It is timing, consent, channel choice, customer context, script control, escalation, payment resolution, and follow-up. If those parts are split across five tools, your team is not running a collections process. They are chasing fragments.

Key Takeaways:

- Payment recovery improves when teams design the workflow around the customer's next action, not the agent's next task.

- The real bottleneck is often handoff quality, not call volume.

- Teams should track right-party contact, promise-to-pay, actual payment, and broken handoffs as separate signals.

- AI should not become another queue. It should reduce queues by sharing context, knowledge, and workflow ownership with human agents.

- If failed calls, manual follow-ups, and payment conversations sit in different tools, collection performance will always have hidden leakage.

Why Payment Collections Break Before the Customer Answers

The Queue Is Not the Workflow

A collections manager opens Monday with a list of accounts, agent capacity, and a target recovery number. The visible work is simple: reach customers, confirm intent, collect payment, escalate exceptions. The hidden work is harder. Someone has to check contact rules, choose the channel, confirm the latest account status, avoid duplicate outreach, update the system, and make sure follow-up actually happens.

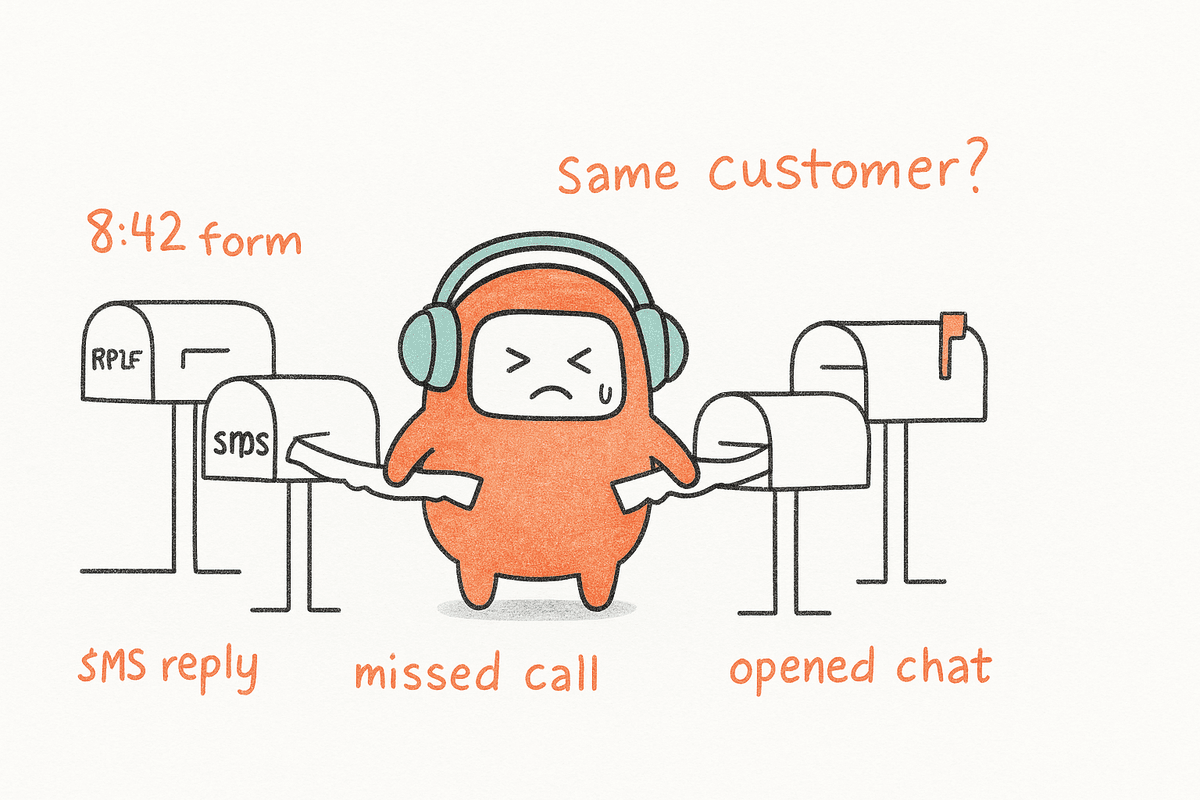

That hidden work is where the cost builds. A customer receives an SMS reminder at 10 a.m., calls back at 2 p.m., and explains the same situation to a human agent who cannot see the AI conversation from the morning. Trust is gone before the payment question is asked. It is like running collections out of a filing cabinet split across five floors. Every folder exists somewhere, but the person on the phone does not have it when the customer is finally ready to act.

More Calls Can Make the Problem Worse

The usual response is to increase outreach volume. More call blocks. More reminders. More agents pulled into recovery campaigns at month-end. I get why teams do it. If the target is missed on Friday, the most obvious answer on Monday is to push more activity through the machine.

That answer has a hard ceiling. If your agents can only process 80 meaningful payment conversations in a shift, sending 300 more contacts into the queue just creates spillover. Customers who need a payment link wait. Customers who need a plan wait. Customers who ask for a person get parked behind routine calls. The team looks busy, but the system is wasting the moments that matter.

The Cost Shows Up as Leakage

Collections leakage is not one giant failure. It is a set of small gaps that repeat all day: the wrong channel, a missed callback, an outdated balance, a handoff without context, a follow-up that goes out too late. Honestly, that is why it is hard to see. The dashboard reports activity, while the real problem hides between activities.

Use a simple diagnostic before adding more volume: count how many reached customers complete the next intended step inside the same workflow. If 100 customers answer and only 38 reach a payment, payment plan, approved dispute path, or human escalation without restarting, the issue is not reach. The issue is workflow completion. Anything below a 60% completion rate on reached accounts means you are paying for outreach you cannot convert.

How to Increase Payment Collections With Workflow Control

To increase payment collections with AI, tighten the workflow before increasing contact volume. The useful question is not "Can AI call more people?" The better question is whether every reached customer can move from contact to resolution without losing context, consent status, or ownership.

Diagnose Where the Payment Moment Falls Apart

Five questions decide whether you have a workflow problem or a reach problem. Can agents see the customer's last message, call attempt, payment status, and prior promise in one place? Can AI and humans use the same approved knowledge and scripts? Can a customer move from call to SMS to human agent without repeating the story? Can your team prove why a message was sent, when it was sent, and what rule allowed it? Can managers separate contact rate from actual payment rate?

Those questions matter because collections teams often measure the wrong middle step. Contact rate is useful, but contact without resolution is just a more expensive queue. Promise-to-pay rate is useful, but a promise that never turns into actual payment is not recovery. For a fast read, pull 50 reached accounts from last week and mark the first broken handoff on each. If more than 15 break between "customer engaged" and "next action completed," your workflow is leaking too much to solve with more outreach. Below 5 breaks, your reach strategy is the bottleneck. Between 5 and 15, both need work but workflow comes first.

Separate Reached Customers From Failed Attempts

Failed attempts and reached customers are two different problems wearing the same dashboard. A no-answer call, bounced message, or wrong-time contact tells you something about reach strategy. A reached customer who does not complete the next step tells you something about workflow quality. Mixing them creates bad decisions and worse meetings.

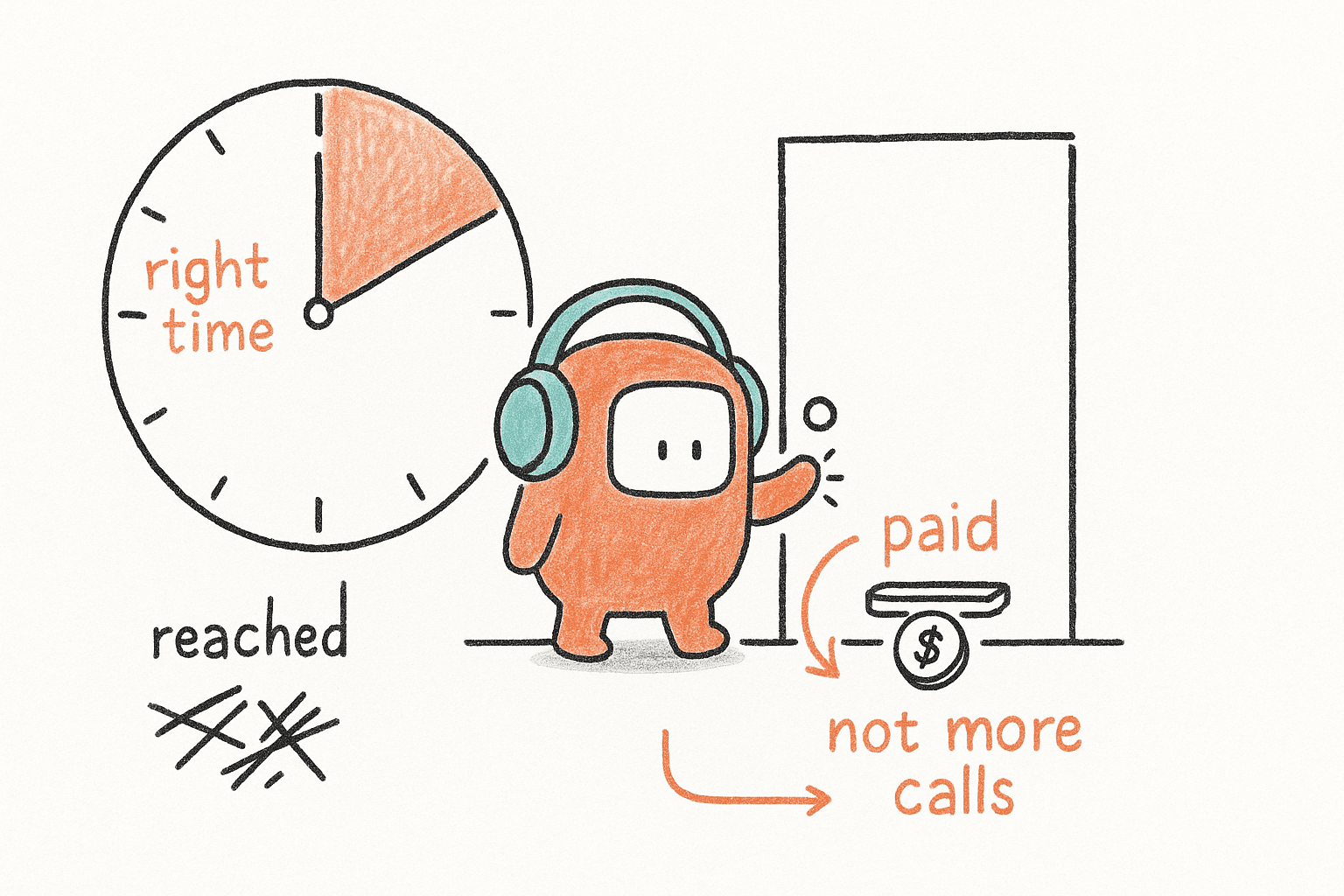

The rule I prefer is simple: optimize failed attempts for timing and channel, then optimize reached customers for resolution. If the customer does not answer, test window, sequence, and channel mix. If the customer answers but does not pay, test script clarity, payment options, escalation, and follow-up timing. That distinction sounds obvious until you sit through a collections review where everything collapses into one "campaign performance" number and nobody can tell whether the issue is dialing or closing.

A useful weekly scorecard has four separate lines:

- Attempt quality: wrong numbers, unreachable contacts, failed connections, and channel limits.

- Right-party contact: reached customers who match the intended account owner or approved contact.

- Resolution path: payment, payment plan, dispute path, callback, or human escalation.

- Completion gap: customers who engaged but did not complete any approved next step.

Build Channel Sequences Around Customer Readiness

Voice, SMS, WhatsApp, email, and messaging are not separate campaigns. Customers move across channels based on convenience and comfort. One customer may ignore two calls but respond to a short message. Another may answer the phone but need a payment link sent immediately. The workflow has to follow that behavior, not the other way around.

A practical sequence starts with the highest-trust contact route, then moves to lower-friction follow-up only when needed. For example: AI call, then SMS payment reminder, then messaging follow-up, then human callback for customers who request help or hit an exception. The order is less important than the memory. If the SMS does not know the call outcome, or the human agent cannot see the prior message, you have built four separate touches instead of one recovery process. The customer feels it on touch two.

Keep Humans Where Judgment Is Required

Automation should take the repetitive work, not the responsibility. A customer who wants to pay but needs a new due date can often move through a defined path. A customer disputing the balance, showing distress, or asking for an exception needs human judgment. Treating both conversations the same is where automation starts to feel blunt.

Set escalation rules before launch, not after the first complaint. If sentiment turns negative, route to a person. If the customer mentions hardship, dispute, legal concern, wrong party, or a payment failure, route to a person. If the conversation exceeds six turns without reaching an approved next step, route to a person. Teams over-automate this part because they want cleaner metrics. Fair enough — escalations look like failures on a dashboard. They are not. An escalation that captures a hardship plan is worth ten clean AI completions that ended in a broken promise next week.

Control Scripts, Consent, and Follow-Up Timing Together

Collections outreach is operationally sensitive because the message, timing, channel, and customer status all matter at once. A script acceptable for one account stage may be wrong for another. A message safe at 2 p.m. may be wrong at 9 p.m. A follow-up that makes sense after a promise-to-pay may be wrong after an opt-out. If those checks live in different places, the team carries risk it cannot see clearly.

The better design places script control, contact rules, opt-out handling, and approval paths inside the same operating flow. Before a message goes out, the system should know whether the customer can be contacted, whether the channel is allowed, whether the script is approved, and whether the agent or AI should pause for review. If your team cannot answer those four questions from a single workflow view, the process is not ready for higher volume. Adding contacts on top of that gap is how regulatory complaints start.

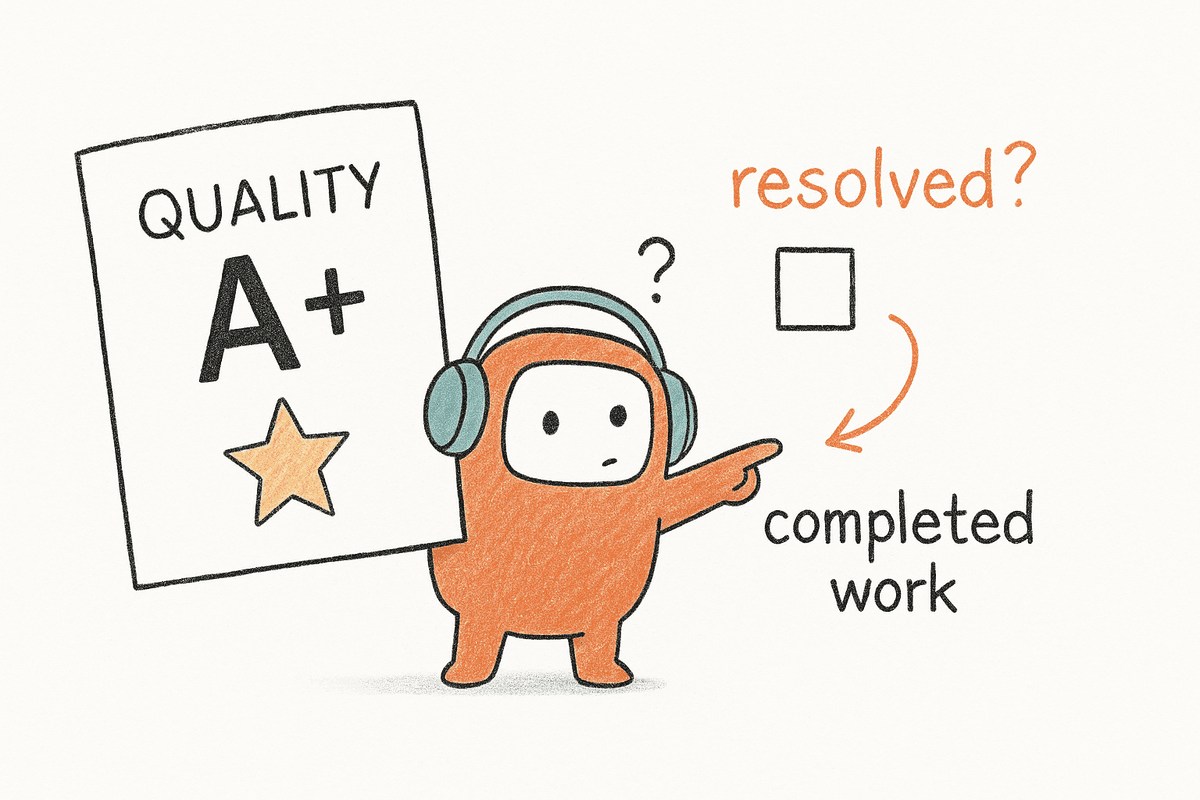

Measure Completed Work, Not Just Activity

Activity can make a collections team feel productive. Completed work proves whether the workflow is working. The difference matters. A thousand calls may look strong in a weekly review, but if the team cannot show how many reached customers moved to payment, plan, dispute review, or human escalation, the number is mostly noise.

The most useful metric stack is small. Track right-party contact, promise-to-pay, actual payment, payment-plan setup, dispute routing, opt-out, and escalation completion. Add one operational number: time from customer engagement to next action completed. If that time is measured in hours, the workflow is too slow. If it is measured in minutes, your team has a chance to recover payments while the customer is still present. For teams reviewing whether their current process can support that kind of handoff, the clean next step is to compare the workflow live with someone who runs collections operations every day — book a demo.

How Revve Runs Collections Workflows

Revve runs collections as a customer operations workflow, not as a standalone dialing task. Outbound outreach, AI voice and text agents, human handoff, knowledge, compliance controls, and conversation history live in one shared workspace. That architecture matters because recovery depends on completed actions, not isolated contacts.

Collections and Payment Recovery With Shared Context

Revve's Collections and Payment Recovery configuration runs AI-led outreach across calls, texts, and messages while keeping the workflow tied to approved scripts, follow-up rules, and customer context. The platform can contact past-due accounts, guide customers toward payment or a payment plan, and escalate complex situations to a person when needed.

The bigger point is control. Collections teams should not run outreach in one system and handle exceptions in another. Revve keeps AI and human agents in the same operating layer, so a customer who moves from automated contact to human support does not have to start over. For collections leaders, that means fewer broken handoffs, cleaner follow-up, and a more realistic view of where recovery actually stalls.

Compliance Controls Without Removing Human Ownership

Revve includes compliance controls and approval workflows for sensitive outreach. Teams configure contact rules, opt-out handling, calling windows, approved scripts, and review paths before campaigns go live. The platform checks those rules before outbound contact or sensitive message delivery, and interactions are logged for review. It gives operations teams a more governable way to run the work.

Revve also supports Smart Escalation and Full-Context Handoff. If a customer asks for a person, hits an exception, shows negative sentiment, or matches a custom escalation rule, the conversation moves to a human agent with the full thread and relevant context attached. The value is not "AI replaces collectors." The value is that repetitive outreach, routine reminders, and structured next steps run consistently, while humans own the conversations that require judgment.

Build Collections Around Work, Not Queues

Payment collections improve when the operating model is built around completed customer actions. Calls, messages, and reminders matter, but only when they connect to payment, plan setup, dispute handling, or human resolution. A collection queue without shared context is just a longer line.

Revve is not for every collections team. If you have low volume, a simple manual process may be easier to run. If you only need a cheap dialer, a point tool may be enough. If you are trying to increase payment collections with AI while managing high conversation volume, channel complexity, consent rules, and human handoff, the architecture matters.

More attempts create more noise. Better workflow creates more recovery.